- January 31, 2023

- Posted by: Murooj Al Alia

- Category: Bookkeeping

It is a holding account for revenues and expenses before they are transferred to the retained earnings account. These permanent accounts form the foundation of your business’s balance sheet. However, you might wonder, where are the revenue, expense, and dividend accounts? These accounts were reset to zero at the end of the previous year to start afresh.

Closing Entries as Part of the Accounting Cycle

A hundred dollars in revenue this year doesn’t count as $100 in revenue for next year even if the company retained the funds for use in the next 12 months. Take note that closing entries are prepared only for temporary accounts. No, permanent accounts carry their balances calculating profits and losses of your currency trades forward to the next accounting period. Revenue, expense, and dividends or withdrawals accounts are closed at the end of an accounting period. After the closing journal entry, the balance on the drawings account is zero, and the capital account has been reduced by 1,300.

How are closing entries posted in the general ledger?

If both summarizeyour income in the same period, then they must be equal. Thebusiness has been operating for several years but does not have theresources for accounting software. This means you are preparing allsteps in the accounting cycle by hand.

How Highradius Can Help You Streamline Your Accounting Management

So, even though the process today is slightly (or completely) different than it was in the days of manual paper systems, the basic process is still important to understand. Closing journal entries are made at the end of an accounting period to prepare the accounting records for the next period. They zero-out the balances of temporary accounts during the current period to come up with fresh slates for the transactions in the next period. The end result is equally accurate, with temporary accounts closed to the retained earnings account for presentation in the company’s balance sheet.

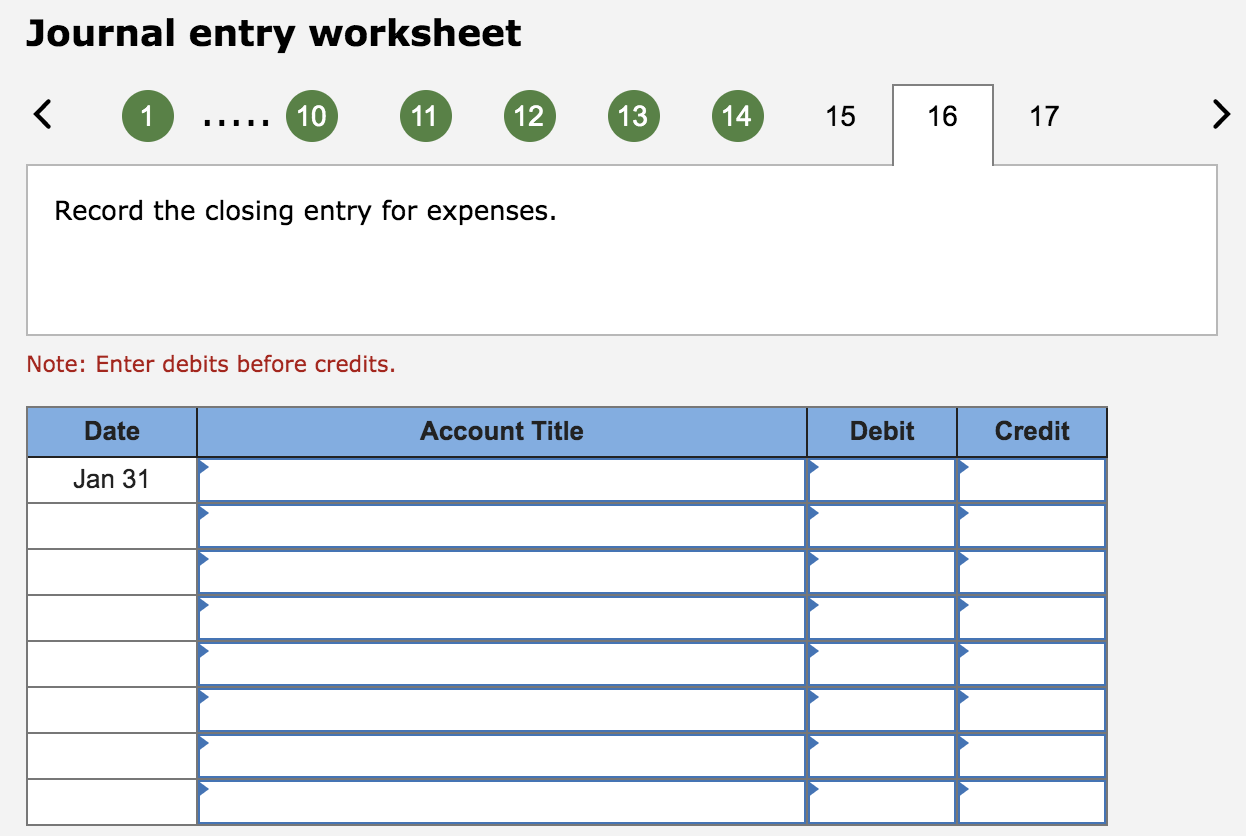

- The second entry requires expense accounts close to the IncomeSummary account.

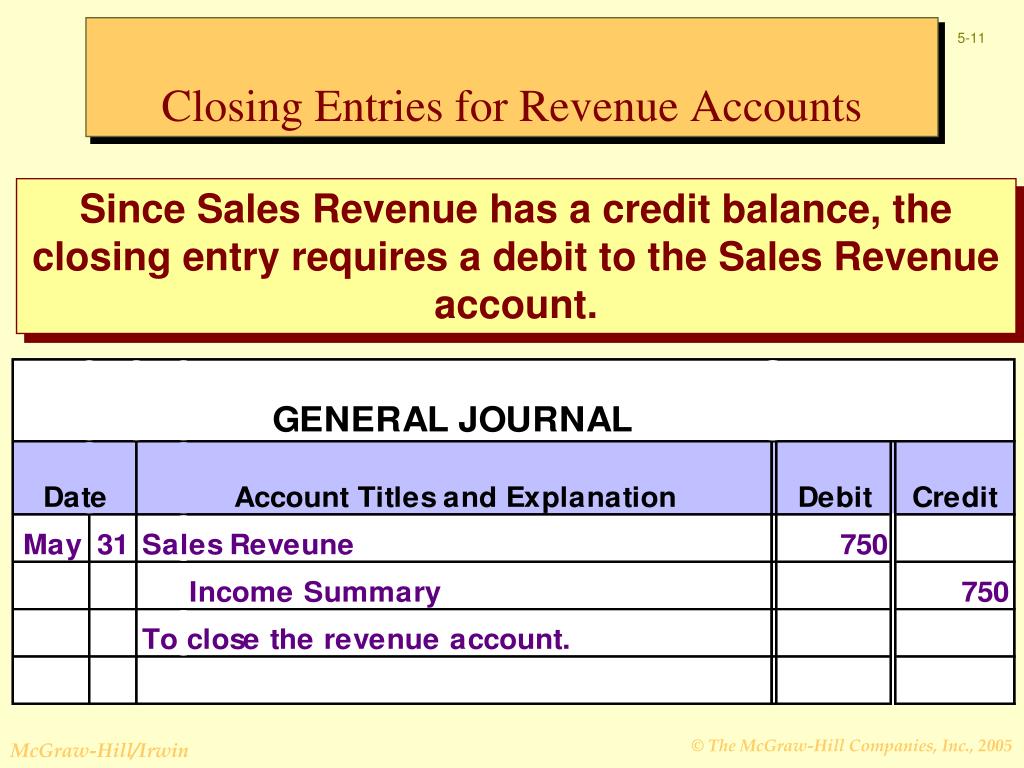

- We know that all revenue and expense accounts have been closed.

- All of these entries have emptied the revenue, expense, and income summary accounts, and shifted the net profit for the period to the retained earnings account.

- Remember, dividends are a contra stockholders’ equity account.It is contra to retained earnings.

FAQs on Closing the Books

According to the statement, the balance in Retained Earnings should be $13,000. The number of closing activities may be quite substantially longer than the list shown here, depending upon the complexity of a company’s operations and the number of subsidiaries whose results must be consolidated. My Accounting Course is a world-class educational resource developed by experts to simplify accounting, finance, & investment analysis topics, so students and professionals can learn and propel their careers.

Step 3: Close Income Summary to the appropriate capital account

In summary, permanent accounts hold balances that persist from one period to another. In contrast, temporary accounts capture transactions and activities for a specific period and require resetting to zero with closing entries. The purpose of closing entries is to prepare the temporary accounts for the next accounting period. In other words, the income and expense accounts are “restarted”.

If dividends were not declared, closing entries would cease atthis point. If dividends are declared, to get a zero balance in theDividends account, the entry will show a credit to Dividends and adebit to Retained Earnings. As you will learn in Corporation Accounting, there are three components to thedeclaration and payment of dividends. The first part is the date ofdeclaration, which creates the obligation or liability to pay thedividend. The second part is the date of record that determines whoreceives the dividends, and the third part is the date of payment,which is the date that payments are made. Printing Plus has $100 ofdividends with a debit balance on the adjusted trial balance.

If we had not used the Income Summary account, we would not have this figure to check, ensuring that we are on the right path. What is the current book value ofyour electronics, car, and furniture? Are the value of your assets andliabilities now zero because of the start of a new year? Your car,electronics, and furniture did not suddenly lose all their value,and unfortunately, you still have outstanding debt. Therefore,these accounts still have a balance in the new year, because theyare not closed, and the balances are carried forward from December31 to January 1 to start the new annual accounting period. The next day, January 1, 2019, you get ready for work, butbefore you go to the office, you decide to review your financialsfor 2019.

The second entry requires expense accounts close to the IncomeSummary account. The accounts that need to start with a clean or $0 balance goinginto the next accounting period are revenue, income, and anydividends from January 2019. To determine the income (profit orloss) from the month of January, the store needs to close theincome statement information from January 2019.